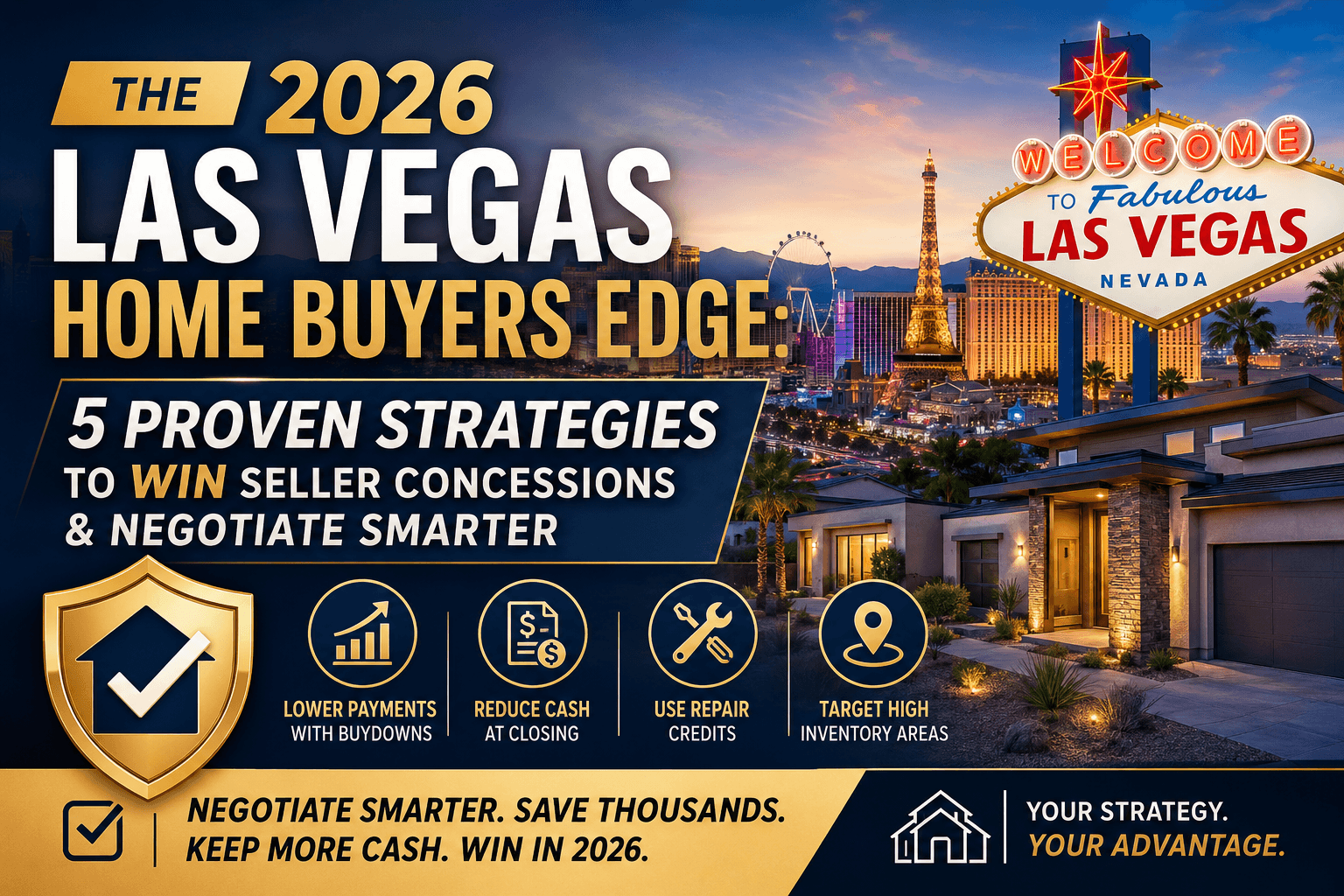

The Las Vegas real estate market is rebalancing in 2026, and seller concessions Las Vegas 2026 give prepared buyers leverage they haven’t seen in years.

Seller contribution limits are set by HUD for FHA loans and by VA for VA loans.

After a period of historically low inventory and multiple-offer situations, we are seeing key shifts across the valley:

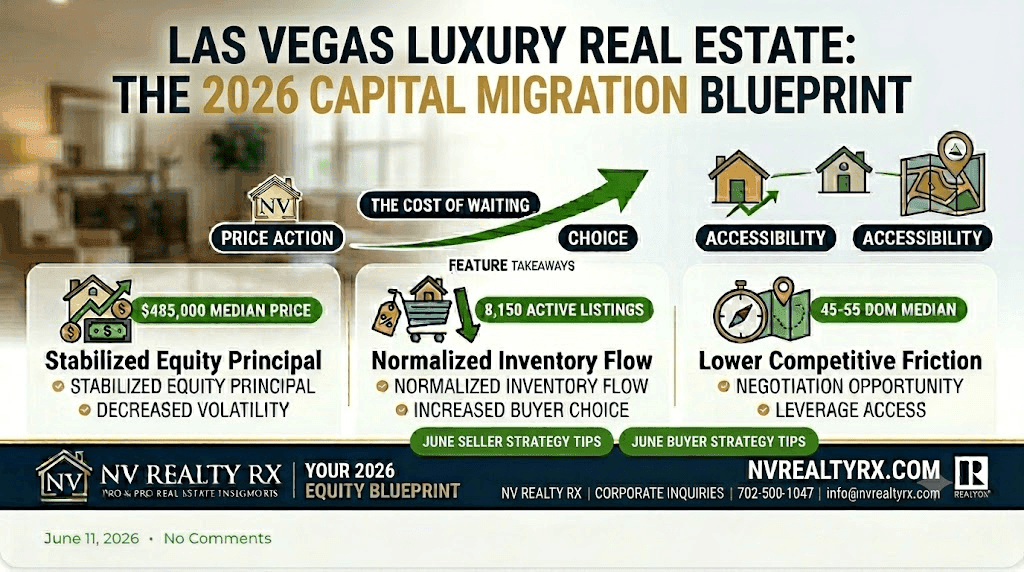

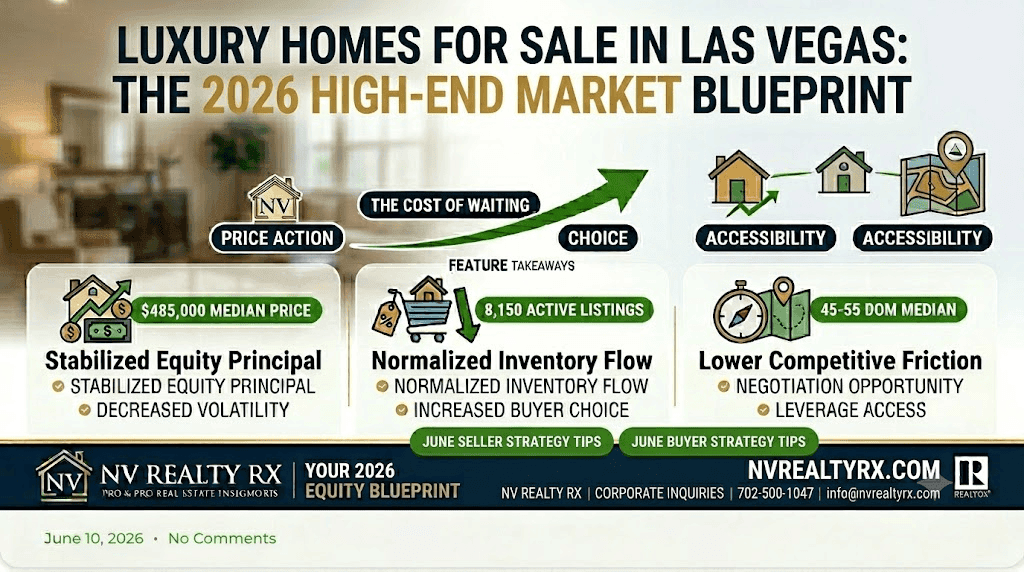

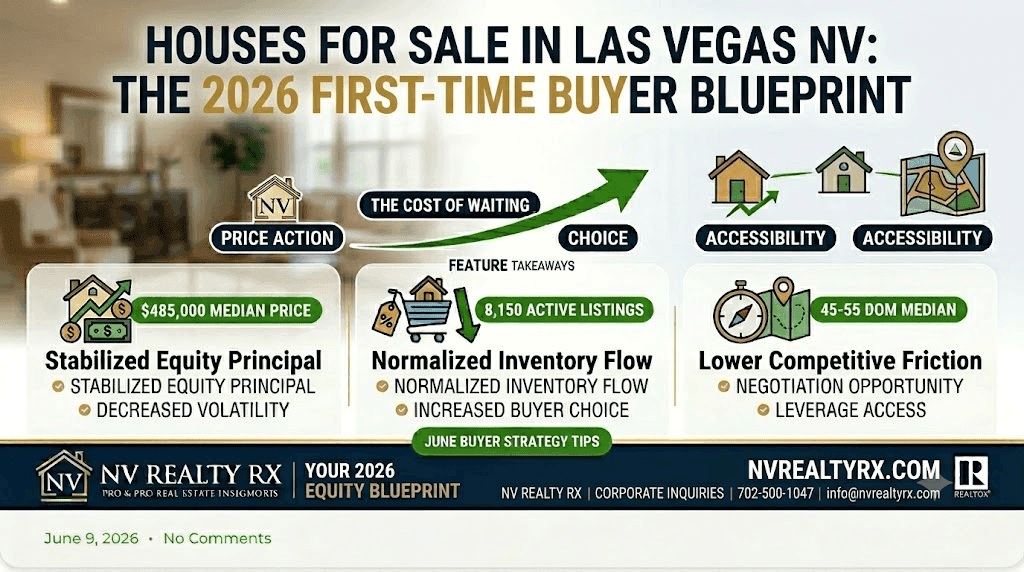

- Inventory is trending up in areas like Summerlin, Henderson, and North Las Vegas compared to 2023-2024 lows

- Price adjustments are more common as homes sit longer than the peak 2021-2022 period

- Days on market have increased in several zip codes, especially for homes priced above $500,000

- Builders and resale sellers are offering incentives to compete for qualified buyers

What this means for you:

The buyer who knows how to structure an offer with seller concessions can save thousands in upfront costs and reduce monthly payments often more effectively than chasing a lower purchase price.

What Are Seller Concessions And Why They Matter in 2026?

Seller concessions are contributions the seller agrees to pay toward the buyer’s costs. They are negotiated into the purchase contract and regulated by your loan type.

Common concession structures in Las Vegas right now:

- Closing cost credits – covers lender fees, title, escrow, prepaid taxes/insurance

- Mortgage rate buydowns – seller funds temporarily lower your interest rate

- Repair credits – cash at closing for you to handle inspection items

Why concessions beat price cuts in a shifting market:

- Preserves your cash for moving, furniture, or reserves

- Lowers monthly payment if applied to a buydown

- Helps you qualify by reducing cash-to-close requirements

Note: All concessions must comply with lender guidelines. Not a commitment to lend. Terms subject to qualification.

1. Reduce Monthly Payments With a 2-1 Mortgage Rate Buydown

A 2-1 buydown is one of the most powerful tools Las Vegas buyers are using in 2026.

How it works:

- Year 1: Your interest rate is 2% below the note rate

- Year 2: Your rate is 1% below the note rate

- Year 3+: You pay the full note rate for the remainder of the loan

Example: On a $450,000 loan at 6.5% note rate, a 2-1 buydown could lower your payment by ∼$500/mo in year 1 and ∼$250/mo in year 2.

Why sellers agree to it:

Funding a buydown costs the seller less than a large price reduction, while keeping the sold price higher for neighborhood comps.

Important to know:

Not all loan programs allow buydowns. Funds must come from an interested party like the seller or builder. If you refinance or sell before year 3, you don’t recoup unused buydown funds.

→ Want to see your exact savings with a seller-funded buydown?

👉 Get a Free Buydown Scenario: Visit staging.nvrealtyrx.com/ or email towanda@nvrealtyrx.com for a custom payment breakdown based on today’s rates.

*For illustration only. Actual savings depend on loan amount, rate, and lender terms.

2. Negotiate Closing Cost Credits Instead of Price Cuts

Closing costs in Clark County typically run 2% – 5% of the purchase price. On a $550,000 Las Vegas home, that’s $11,000–$27,500 due at closing.

Smarter negotiation:

Instead of “Please reduce price by $15,000, ask:

“Seller to contribute $15,000 toward buyer’s closing costs and prepaids.

Why this wins:

- You keep cash in your pocket for reserves, upgrades, or rate buydown

- Stronger offer – sellers net similar proceeds but your offer stands out vs. buyers who need price cuts

- Appraisal safety – you’re not pushing the contract price below appraised value

This strategy is especially effective for first-time buyers and VA/FHA buyers who want to limit out-of-pocket expenses.

3. Use Repair Credits Instead of Asking Sellers to Fix Issues

Inspection reports in Las Vegas often flag:

- Aging HVAC units stressed by summer heat

- Roof wear from sun/thermal expansion

- Deferred maintenance on pools or landscaping

Best practice in 2026: Request a repair credit at closing instead of requiring the seller to complete repairs.

Advantages for you:

- Control quality: You choose licensed contractors, not the cheapest fix

- Avoid delays: No waiting on seller repairs to close

- Negotiating power: Sellers prefer credits vs. managing vendors

Pro tip: Have your agent get contractor bids during the inspection period so your credit request is backed by real numbers.

4. Target High-Inventory Las Vegas Areas for Maximum Leverage

Not every zip code negotiates the same. In 2026, buyer leverage is strongest where supply has increased most.

Where concessions are most common right now:

- North Las Vegas & Centennial Hills: New construction competition + resale inventory growth

- Southwest & Mountains Edge: High turnover from 2020-2022 buyers gaining equity to move

- Henderson – Cadence & Inspirada: Builders offering aggressive incentives to move standing inventory

- Skye Canyon & Providence: Longer days on market above $600k price point

Builder incentives to watch in 2026:

- Interest rate buydowns to 4.99%–5.5% range*

- $10k–$25k toward closing costs

- Design center credits for flooring/upgrades

Important: Builder contracts are different from resale. Some incentives require using preferred lenders or title. A local agent protects you from hidden trade-offs.

→ Want a map of Las Vegas concession-friendly neighborhoods?

👉 Get Your Free 2026 Hot Zone List: Text “CONCESSIONS” to 702-500-1047 or visit staging.nvrealtyrx.com/. We’ll send current inventory + incentive trends by zip code

5. Understand Seller Concession Limits by Loan Type

The biggest deal-killer? Asking for concessions above what your loan allows. Here are 2026 general guidelines:

| Loan Type | Max Seller Concession | Notes |

| Conventional | 3%–9% of price | Depends on down payment: 3% if <10% down, up to 9% if ≥25% down |

| FHA | Up to 6% | Cannot be used for down payment |

| VA | Up to 4% for concessions | Plus seller can pay all “customary” closing costs |

| USDA | Up to 6% | Rural areas outside Las Vegas metro |

Why this matters:

If your contract exceeds limits, the lender will reduce the concession and you’ll need to bring more cash to close. A skilled agent structures the offer to maximize allowable credits without triggering underwriting issues.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}